For years, many Malaysian taxpayers viewed dividend income as a secondary “informational” detail—a figure tucked away in the back of the mind and the tax return, rarely moving the needle on the final amount owed to the Inland Revenue Board (LHDN). However, as we approach the filing season for the Year of Assessment (YA) 2025, that era of passive reporting has come to a definitive end.

While tax season is often regarded as a routine exercise in data entry, the updates to Form B and Form BE represent a critical turning point. With the introduction of the new Dividend Tax and specific residential property reliefs, individual filers can no longer afford to treat their tax returns as “business as usual.” This year, your dividend portfolio is no longer just a disclosure; it is a primary calculation that could significantly impact your liquidity.

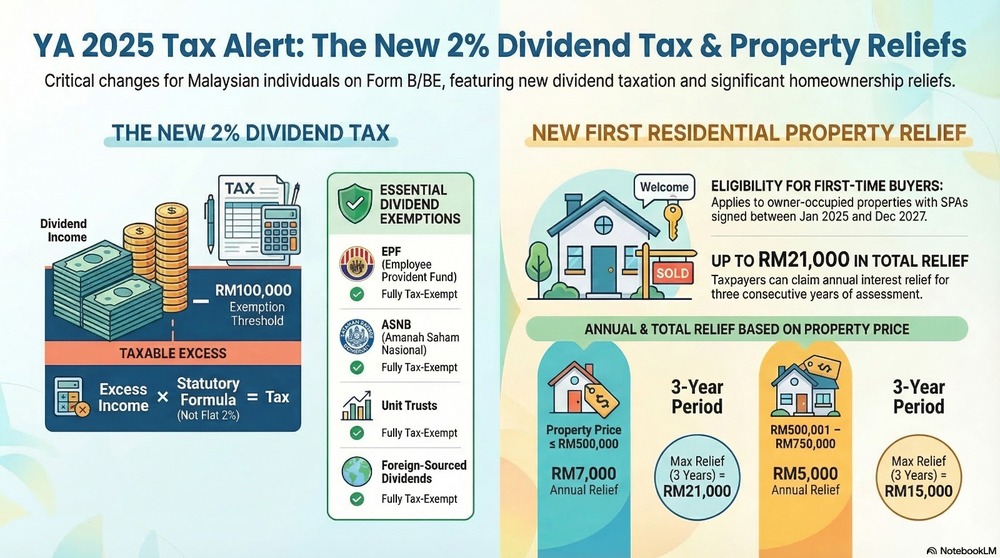

1. Dividends are No Longer Just “Informational”

The most striking change in the YA 2025 tax forms is the elevation of dividend income from the sidelines to the main stage. In Form B, taxpayers will find a brand-new line item—Item B8: Statutory Income from Dividends. Similar updates have been integrated into Form BE, including specific columns to capture spouse dividends for those filing under joint assessment.

This structural change signals that dividend income now directly dictates your tax payable. As noted in recent guidance:

“This is not a cosmetic change—incorrect reporting may result in additional tax, penalties, or audit queries.”

Treating these new columns as optional or “background noise” is a risk no taxpayer should take. The system is now engineered to capture and tax dividend wealth that exceeds specific thresholds, making technical accuracy the new standard for compliance.

2. The “Simple 2% Math Trap”

At first glance, the new policy appears straightforward: Malaysian-sourced dividends exceeding RM100,000 are subject to a 2% tax. However, sophisticated taxpayers must avoid the “simple math trap.” This is not a flat 2% levy on the excess amount. Instead, the tax is integrated into your broader financial position using a statutory formula:

Chargeable Dividend Income = (Statutory Dividend Income ÷ Aggregate Income) × Chargeable Income

To see this in action, imagine a taxpayer with RM300,000 in employment income and RM250,000 in Malaysian dividends. After the RM100,000 exemption, the Statutory Dividend Income (A) is RM150,000. If the total Aggregate Income (B) is RM450,000 and the Chargeable Income after reliefs (C) is RM441,000, the calculation is:

(150,000 ÷ 450,000) × 441,000 = RM147,000 (Chargeable Dividend Income)

The 2% tax is then applied to that RM147,000, resulting in RM2,940.

There are two critical “negatives” every filer must understand:

- No Withholding Tax: Companies will not deduct this 2% at the source. You are responsible for setting aside the cash to pay this bill.

- No Tax Credits: Unlike the old “set-off” system, there are no tax credits available to buffer this cost. It is a pure additional expense.

However, there is a subtle “human-readable” benefit to this formula. By using “Chargeable Income” (the figure after all your personal reliefs) as a multiplier, the system ensures that your lifestyle, medical, and education reliefs actually help reduce your dividend tax liability. The more reliefs you claim, the lower your dividend tax becomes.

3. Not All Dividends are Created Equal (The Safe Zones)

To avoid overpaying, you must distinguish between taxable dividends and those that remain in the “safe zone.” Reporting exempt dividends as taxable is a common error that leads to an inflated tax bill—a mistake LHDN is unlikely to correct on your behalf.

Common Institutional Dividends (Exempt):

- EPF (KWSP), ASNB, and LTAT

- Unit trust distributions

Specific Corporate and Specialized Dividends (Exempt):

- Dividends from companies with Pioneer Status or Reinvestment Allowances

- Shipping companies and Cooperatives

- Closed-end funds and Labuan entities

The Foreign Income Exception: Foreign-sourced dividends remain a significant safe zone for individual taxpayers, as they are currently exempt from this specific tax until YA 2036.

The Golden Rule: Never mix exempt and taxable dividends in your computation. Keep them strictly segregated to ensure you aren’t paying 2% on income that the law intends to protect.

4. A Silver Lining for First-Time Homebuyers

While the dividend tax adds a new layer of complexity, the 2025 updates aren’t exclusively about tightening belts. There is a significant incentive for first-time homebuyers who signed their Sale and Purchase Agreements (SPA) between January 1, 2025, and December 31, 2027.

The “First Residential Property Interest Relief” provides a deduction for interest paid on housing loans for owner-occupied properties for up to three consecutive years. It is important to note that this is a tax relief (a deduction from your total income), not a direct cash rebate or tax credit.

| Property Price | Annual Tax Relief (Deduction) | Max Relief Over 3 Years |

| RM500,000 or below | RM7,000 | RM21,000 |

| RM500,001 – RM750,000 | RM5,000 | RM15,000 |

5. Actionable Conclusion: The Compliance Mindset

The landscape of Malaysian personal taxation has shifted from simple reporting to complex optimization. For YA 2025, your primary directive is clear:

- Meticulous Review: Audit your dividend vouchers now. Distinguish between taxable corporate dividends and exempt institutional distributions.

- Joint Assessment Alignment: If you file jointly, you must carefully coordinate with your spouse. The new dividend columns appear on both Form B and BE, and inconsistencies between spouses are a red flag for auditors.

- Documentation is King: Retain all dividend certificates and create audit-ready tax computation files. Under the new formulaic approach, being able to justify your “Statutory Dividend Income” is the only way to protect your position.

As the line between “exempt” and “taxable” income continues to blur, the burden of proof rests entirely on the taxpayer. Are your records robust enough to withstand a 2026 audit?

Strengthen your tax strategy and stay ready for change with corporate tax planning in Selangor tailored to support better business decisions.

Get in touch with NKH to stay updated on the latest tax changes and receive practical guidance for smarter tax planning.

Kim Heng is an accounting and taxation professional whose sterling reputation has drawn countless clients to the NKH Group. When the GST was first introduced, he was commissioned to give 100+ talks on GST implementation as well as over 20++ talks on E- Invoice implementation by multiple businesses and industry associations, showing the depth of their confidence in his expertise. In the following years, Kim Heng would go on to share his knowledge on (among others) branding, tax planning, and fundraising at 20+ seminars organised by business associates that were widely attended by the public. He has over 20 years of experience consulting and advisory on taxation, corporate structure planning, business valuer, company secretarial administration, constitution advisory, and etc.